🤖 EA name:

1) Atlas Fluxo Quant EA

2) Darker EA

3) Dual-Trendline Breakout Scalper EA

Friends, we want to show you a great example of the importance of testing algorithms on the highest quality tick data using real spread.

💻 Platform: MT4

⚠️ Attention: Recommended best VPS, BROker

🏛 Tick Data Provider: Darwinex (TDSv2)

🧭 GMT: +2; DST: US

Real spread: ✅

Slippage: ❌

📌 All EAs tests EA ForexLab

In order to download an adviser with tests, go to our telegram channel 👇

A bad backtest is not just a weak trading result. In automated trading, a bad backtest can be a warning sign that the Expert Advisor has no real statistical edge, is too sensitive to market conditions, or was promoted using selective results that do not survive more realistic testing.

This article reviews three Expert Advisors that produced poor or highly questionable results in independent Strategy Tester reports:

- Atlas Fluxo Quant EA

- Darker MT4

- Dual-Trendline Breakout Scalper EA Update

The goal is not to attack any developer or vendor. The goal is to show traders how to read bad EA tests correctly and avoid trusting marketing claims without independent verification.

All three reports were tested in MetaTrader using the “Every tick” model, 99.90% modelling quality, variable spread, and a $1,000 initial deposit. The results are not marginally disappointing. They show deep structural problems: negative expectancy, extreme drawdown, weak profit factor, poor risk-adjusted behavior, and in some cases a complete collapse of the equity curve.

Why Bad EA Backtests Matter

Most traders do not lose money because they cannot find profitable-looking robots. They lose money because they cannot distinguish between a real trading edge and a backtest illusion.

The Expert Advisor market is full of attractive claims: advanced algorithms, quantitative modelling, AI logic, non-linear formulas, professional risk management, no grid, no martingale, safe scalping, stable growth, and optimized set files. These phrases sound convincing, but they do not prove anything.

A strategy must survive objective testing.

A serious EA review should not ask only:

“Did the robot make money in one backtest?”

It should ask:

“How was the money made, what risk was required, and does the system still look viable when tested under realistic conditions?”

This is especially important because some Expert Advisors may be heavily optimized for a narrow historical period. In more suspicious cases, the EA may use hidden filters, hardcoded dates, or specific calendar logic to avoid known losing periods in history. Our article about the 28-year shift test explains this problem well: a smooth backtest may become unreliable if the EA depends on exact historical dates or hidden time-based rules.

A failed backtest does not automatically prove manipulation. But it does prove one thing: the trader should not trust the product without deeper validation.

Test Summary: Three EAs, Three Forms of Failure

The three tested systems failed in different ways.

Atlas Fluxo Quant EA produced a direct, clean failure: negative profit, extremely low win rate, and a downward equity curve.

Darker MT4 produced a more deceptive failure: a high win rate, thousands of trades, and yet still a negative final result because the average loss was much larger than the average win.

Dual-Trendline Breakout Scalper EA Update produced the most dangerous type of result: almost breakeven net profit with catastrophic drawdown. This is not a profitable system with volatility. It is a system that nearly destroyed the account to end almost flat.

These are three different examples of why headline descriptions from vendors or resellers should never replace independent testing.

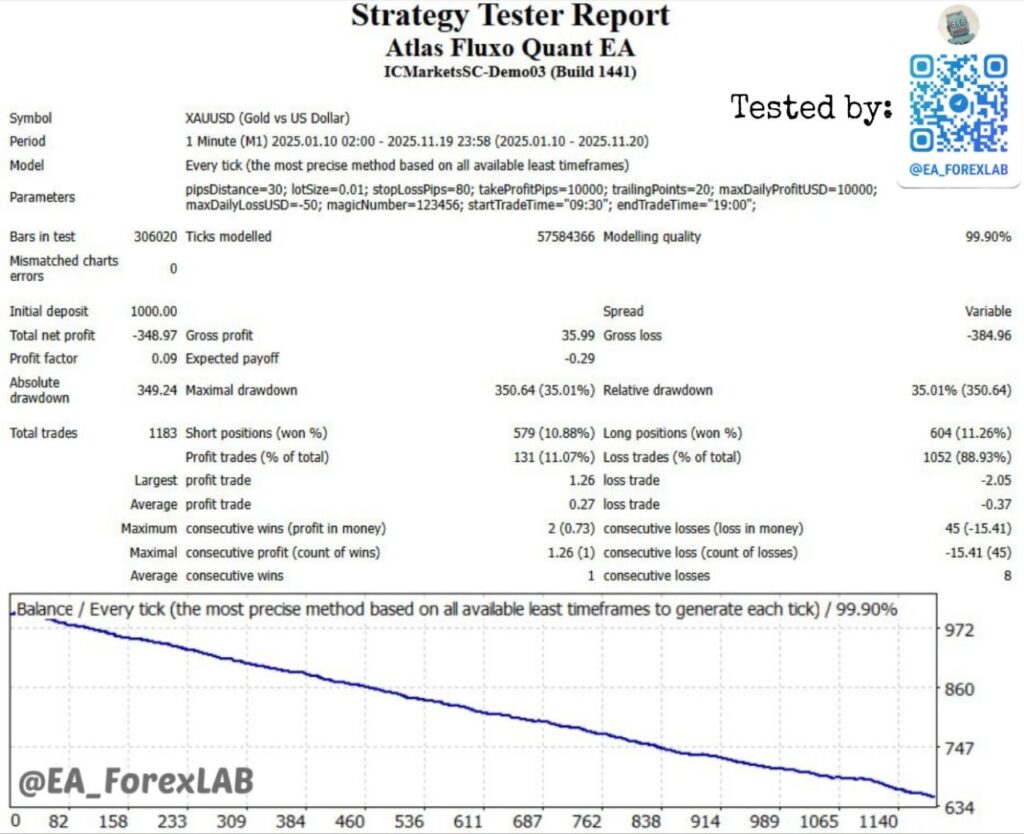

Atlas Fluxo Quant EA: A Backtest That Fails Directly

Atlas Fluxo Quant EA was tested on XAUUSD M1 from 2025.01.10 to 2025.11.19, using variable spread and 99.90% modelling quality. The test produced:

- Total net profit: -$348.97

- Profit factor: 0.09

- Expected payoff: -$0.29

- Relative drawdown: 35.01%

- Total trades: 1,183

- Win rate: 11.07%

- Loss trades: 88.93%

These numbers are not simply weak. They are structurally unacceptable.

A profit factor of 0.09 means the system produced only nine cents of gross profit for every dollar of gross loss. This is not a small edge that failed due to bad luck. This is a deeply negative trading profile.

The win rate is also extremely poor. Only 11.07% of trades were profitable, while nearly 89% were losing trades. That would only be acceptable if the average winning trade were many times larger than the average losing trade. But that is not the case. The average profit trade was only $0.27, while the average loss trade was -$0.37.

That means the EA had neither a high win rate nor favorable payoff asymmetry. It lost often, and its winners were not large enough to compensate.

This is one of the clearest possible signs of a strategy with no visible statistical edge in the tested conditions.

The Vendor-Style Claim vs the Test Reality

Online product pages and reseller descriptions around Atlas Quant / Atlas Fluxo Quant style EAs often use language such as “quantitative modelling,” “volatility mapping,” “trend response logic,” and “professional-grade” automated trading. Some pages describe Atlas-style systems as designed for XAUUSD with advanced quantitative logic and structured execution.

That kind of language creates an impression of sophistication. But the independent test does not confirm a working edge.

A serious trader should ignore the branding and focus on the actual distribution of results. In this test, Atlas Fluxo Quant EA did not merely underperform. It generated a persistent downward balance curve and finished with a substantial loss relative to the $1,000 starting deposit.

The most important conclusion is simple:

A robot can sound quantitative and still fail completely when tested with realistic spread conditions.

Darker MT4: The High-Win-Rate Trap

Darker MT4 is more interesting because its failure is less obvious to inexperienced traders.

The test was run on EURUSD M5 from 2020.01.10 to 2026.02.20, with 99.90% modelling quality and variable spread. The report shows:

- Total net profit: -$377.37

- Profit factor: 0.91

- Expected payoff: -$0.07

- Relative drawdown: 41.26%

- Total trades: 5,223

- Win rate: 77.98%

- Average profit trade: $0.92

- Average loss trade: -$3.59

At first glance, a 77.98% win rate may look attractive. This is exactly the trap.

A high win rate does not automatically mean a profitable strategy. Darker MT4 won most of its trades, but the average losing trade was almost four times larger than the average winning trade. That imbalance destroyed the statistical value of the win rate.

This is a classic retail EA problem: many small wins create psychological comfort, but larger losses quietly erase the gains.

Why Profit Factor Below 1 Is a Red Line

A profit factor below 1.00 means gross losses exceed gross profits. In this test, Darker MT4 generated $3,749.57 in gross profit but -$4,126.94 in gross loss. The final result was negative despite more than five thousand trades.

This matters because 5,223 trades is a large sample. A small sample can be noisy. But when a system runs thousands of trades and still produces a negative expectancy, the result is harder to dismiss as random variation.

The expected payoff of -$0.07 per trade confirms the same issue. Every trade, on average, had a negative contribution to the account.

Vendor Claims vs Independent Test

Darker MT4 is promoted on MQL5 as using a “unique non-linear formula” for calculating entries and a unique algorithm for fixing results. The MQL5 page lists the product by Evgeniy Zhdan and describes its entry logic in proprietary terms.

Other reseller pages describe Darker MT4 as a professional EA with fixed SL/TP, spread control, minimal settings, stable performance, and disciplined risk management. Some even frame it as suitable for traders seeking conservative automation.

The independent test does not support that optimistic interpretation.

The EA lost money, produced more than 41% relative drawdown, and failed to convert a high win rate into profitability. A robot with 78% winning trades but negative expectancy is not conservative. It is structurally weak.

The key lesson:

Win rate is one of the most abused metrics in EA marketing. Without average win, average loss, profit factor, and drawdown, it means very little.

Dual-Trendline Breakout Scalper EA Update: The Most Dangerous Test

Dual-Trendline Breakout Scalper EA Update produced the most alarming report in this comparison.

The EA was tested on XAUUSD M15 from 2020.01.13 to 2026.02.20, using variable spread and 99.90% modelling quality. The result:

- Total net profit: $31.55

- Profit factor: 1.00

- Expected payoff: $0.01

- Relative drawdown: 97.43%

- Maximal drawdown: $1,130.64

- Total trades: 3,643

- Win rate: 81.39%

- Average profit trade: $4.04

- Average loss trade: -$17.62

This is not a good test. It is a near-death equity curve that ended almost flat.

The most important number is not the final profit. The most important number is 97.43% relative drawdown. That means the account was practically destroyed during the test. A system that nearly wipes out the account to finish with $31.55 profit on a $1,000 deposit is not robust. It is unusable for any trader who cares about risk control.

Profit Factor 1.00 Means No Meaningful Edge

A profit factor of 1.00 is essentially breakeven before considering real-world trading degradation. The EA generated $11,980.10 gross profit and -$11,948.55 gross loss. That is an enormous amount of trading activity for almost no net result.

This is a classic churn profile: the robot moves a lot of money through the account, but almost none of it remains as profit.

Even worse, the average loss trade was -$17.62, while the average profit trade was only $4.04. That means one average loss erased more than four average wins. The EA compensated with an 81.39% win rate, but the risk/reward structure remained fragile.

When this type of system meets a bad market phase, the damage can be severe.

The Marketing Conflict

Dual-trendline breakout scalpers are usually marketed around clean concepts: XAUUSD focus, M15 timeframe, trendline confirmation, breakout filtering, stop-loss protection, and no grid or martingale. Some pages around Mon Scalper / Dual-Trendline style systems describe the strategy as gold-specific, based on dual-trendline breakout confirmation, and positioned as transparent or safe.

The tested report does show some structural consistency with that theme: XAUUSD, M15, “Mon Scalper” in the comment field, breakout-style pending orders, stop-loss logic, trailing parameters, and trendline-related settings.

But the result is not safe.

A 97.43% relative drawdown is not a minor weakness. It is an existential failure. If a trader used this EA on a real account with similar conditions and similar risk, the account could have been effectively wiped out before the final recovery.

This is the kind of backtest that can deceive people if they look only at the final line and ignore the equity curve.

The key lesson:

A small final profit does not matter if the system nearly destroys the account to get there.

What These Three Bad Tests Have in Common

Although the three systems behave differently, the reports share several important warning signs.

1. The Equity Curves Do Not Support Trust

Atlas Fluxo Quant shows a clear downward curve. Darker MT4 shows a long deterioration despite many trades. Dual-Trendline Breakout Scalper shows severe instability and near-total drawdown before ending almost flat.

A good EA does not need a perfect equity curve, but it must show a relationship between return and risk that makes sense. These tests do not.

2. Profit Factor Is Weak or Meaningless

Atlas Fluxo Quant: 0.09

Darker MT4: 0.91

Dual-Trendline Breakout Scalper: 1.00

A profit factor below 1 means the system lost money. A profit factor around 1 means there is no meaningful edge. In real trading, where slippage, commissions, liquidity, execution delay, and broker-specific conditions matter, a system with profit factor near 1 is usually not acceptable.

3. Expected Payoff Is Negative or Almost Zero

Atlas Fluxo Quant: -$0.29

Darker MT4: -$0.07

Dual-Trendline Breakout Scalper: $0.01

Expected payoff tells us how much the system earns or loses per trade on average. These values are either negative or statistically insignificant. A real trading system needs enough edge to absorb future degradation. These EAs do not show that cushion.

4. High Win Rate Does Not Save a Bad Strategy

Darker MT4 and Dual-Trendline Breakout Scalper both show high win rates. But both also show poor risk/reward structures.

This is why win rate should never be used alone. A system can win 80% of the time and still be dangerous if the losing trades are much larger than the winning trades.

5. Vendor Language Should Not Replace Independent Testing

Marketing pages often use terms like “professional,” “safe,” “quantitative,” “advanced,” “stable,” “breakout confirmation,” and “risk management.” These words may describe the intended concept, but they do not verify the performance.

The only serious approach is to test the EA independently, with real tick data, variable spread, multiple periods, multiple brokers if possible, and forward validation.

How These Results Relate to Backtest Manipulation Risk

Not every bad result indicates fraud. Sometimes the EA is simply weak. Sometimes the set file is poor. Sometimes market conditions changed. Sometimes the vendor’s original backtest used different broker data, spread, commission, GMT offset, or risk settings.

However, the broader issue is that many commercial EAs are sold using polished backtests that traders cannot easily reproduce.

This is why backtest integrity checks matter.

In the article on detecting hardcoded dates in Expert Advisors, the key idea is that a beautiful backtest is only the beginning. If an EA is robust, its general behavior should remain reasonably stable when tested outside its most convenient historical setup. If the result collapses after a date shift or a minor testing change, the original backtest should not be trusted on its own.

The same principle applies here.

These three tests show that when conditions are less promotional and more objective, the systems do not justify confidence. Whether the cause is overfitting, weak logic, poor execution sensitivity, bad settings, or misleading marketing, the practical conclusion is the same:

Do not trade these results on a live account without deeper validation.

What a Trader Should Do Before Trusting Any EA

Before using any commercial Expert Advisor, traders should follow a strict due diligence process.

First, test the EA using high-quality tick data and variable spread. Fixed-spread backtests can be misleading, especially for scalpers and gold robots.

Second, check the relationship between profit factor, drawdown, expected payoff, and average trade. Do not trust net profit alone.

Third, review the equity curve. A strategy that survives through huge drawdown or late recovery is not reliable just because the final balance is positive.

Fourth, run multiple test periods. If the EA works only in one carefully selected period, the edge may be overfit.

Fifth, test different broker conditions. Spread, commission, GMT offset, execution model, and session data can all change the result.

Sixth, forward test the EA before risking meaningful capital. A demo account is not identical to live trading, but it is still an important filter before real-money exposure.

Seventh, consider robustness tests such as date-shift testing, out-of-sample checks, and parameter sensitivity analysis.

If the EA fails these checks, it should not be treated as a proven trading system.

Final Verdict

The three tested Expert Advisors show different versions of the same core problem: attractive product descriptions do not guarantee a tradable edge.

Atlas Fluxo Quant EA failed directly. The test showed negative profit, extremely low win rate, poor expectancy, and a clear downward equity curve. This is the weakest statistical profile in the group.

Darker MT4 failed more subtly. It produced a high win rate and thousands of trades, but the average loss was much larger than the average win. The result was negative expectancy, negative net profit, and more than 41% relative drawdown.

Dual-Trendline Breakout Scalper EA Update produced the most dangerous backtest. It ended with a tiny profit, but only after a catastrophic 97.43% relative drawdown. That is not a successful test. It is a warning sign.

The professional conclusion is clear:

None of these three reports supports live trading confidence.

A trader should not rely on vendor screenshots, reseller claims, or polished descriptions. The real test is whether the EA can produce a stable risk-adjusted result under realistic conditions. In these reports, the answer is no.

For practical traders, the lesson is simple:

A bad backtest is not something to explain away. It is a filter. If the robot cannot survive objective testing, it should not be trusted with real capital.