Subscribe to our channel, here you will find the best 👇

Understanding why forward testing an expert advisor is important is one of the most useful mindset shifts in algorithmic trading. Many traders follow the same path. First comes an idea. Then comes a beautiful backtest. After that, there is optimization, a strong parameter set, an impressive equity curve, and the feeling that the system is almost ready for a live account. That is exactly where a dangerous illusion often appears: the belief that the strategy tester has already provided enough proof.

In practice, it has not.

Why forward testing an expert advisor is important becomes clear the moment you realize how much distance exists between a strong historical result and real trading. In a backtest, the strategy lives inside a model. In live trading, it meets execution delays, missed ticks, platform differences, changing market regimes, broker infrastructure, and all the details that a strategy tester either simplifies or does not reproduce fully.

From a mature trading perspective, forward testing is not a decorative step after optimization and it is not a nice report for self-confidence. It is a test of whether the strategy can survive after leaving the strategy tester and entering a live environment.

Why a Backtest Alone Is Not Enough

The main problem with a good backtest is that it creates confidence too early. This is especially dangerous when an expert advisor shows a smooth curve, low drawdown, and steady growth. Even a strong historical result still does not answer the most important question: will the logic of the system survive outside the training period?

That is where forward testing becomes essential.

It helps answer whether the strategy has transferability. In other words, does it work not only on the section of history used for parameter selection, but also on the next section that was not used in development? If a system looks convincing on historical data and then quickly falls apart on the next segment, that is a strong sign of overfitting, weak structure, or a strategy that depends too heavily on one market regime.

In practical terms, forward testing does not confirm a strategy once and for all. It does something more modest but much more useful: it shows whether there are enough reasons to keep trusting the system after it leaves the comfortable part of history.

A beautiful backtest usually answers only one question: what would have happened inside the model?

Forward testing begins to answer a much harder question: what happens when the model ends?

What Forward Testing Actually Verifies

Many beginners think forward testing is only about one thing: whether the strategy makes money or loses money on the next period. In reality, it shows far more than that.

First, it shows whether the expert advisor was too heavily fitted to historical data. This is the most basic level. If the system cannot hold itself together on the next period after optimization, there is very little reason to trust that parameter set.

Second, forward testing shows how well the strategy’s behavior transfers from the strategy tester into the live environment. This is where things become much more interesting, because in real trading it is not only the market idea that matters. The engineering implementation matters too.

Third, forward testing shows how dependent the strategy is on specific infrastructure: the broker, the server, the symbol, the platform, tick quality, execution mode, VPS conditions, and even trading hours. This is especially important in cases where it first looks like “the market changed,” but the real issue is the environment where the strategy was deployed.

That is why forward testing is not only a profitability check. It is also a test of whether the research process itself has misled the trader.

Forward Testing Shows Tradability, Not Just Profitability

This is one of the most important practical conclusions and deserves to be stated directly.

Many traders look at forward testing as a mini-exam in profitability: did the expert advisor make money on the next segment or not? A more mature view is different.

Forward testing shows tradability better than it proves theoretical truth.

That is a subtle but critical difference. Forward testing does not mathematically prove that a strategy has a permanent edge. What it shows is something more practical: can this strategy actually be traded in a live environment without its logic being destroyed?

A strategy can look elegant in the tester and logical on paper, but still be poorly tradable under real conditions. If its advantages disappear because of spread, rejects, delays, tick structure, or platform behavior, then in practice it is not a workable trading system, even if the model looked convincing.

That is exactly why forward testing an expert advisor is important before live trading. It is not only about future PnL. It is about whether the strategy can exist as a real operating system in the market rather than as a good-looking idea in a tester report.

Why Matching Live EA Behavior to the Strategy Tester Matters

This is probably the strongest engineering principle behind the entire topic.

Inside the strategy tester, everything looks clean. The required ticks arrive, the logic is processed, the reversal happens where it should happen, and exits occur under the conditions the developer intended. On a live account, that correspondence can break.

And that leads to an uncomfortable but important conclusion: if the live expert advisor does not behave the same way as the tester model, then comparing backtest results to live results becomes only partially meaningful.

At that point, the issue is no longer just whether the strategy is good or bad. The problem is that one object was researched, but a somewhat different object is actually trading.

This is another reason why forward testing an expert advisor is important. It helps verify the quality of the transition from the tester environment to the live trading environment. It reveals whether the strategy’s logic is still intact after deployment.

If the live system begins reacting differently to ticks, entering differently, exiting differently, handling reversals differently, or behaving differently in critical moments, then the question becomes wider: can you still trust the tester results as a valid reference for this implementation?

Missed Ticks, Reversals, and Trading Path Divergence

One of the most underestimated technical problems is that the real trading path can start diverging from the modeled path not because the market changed, but because of small technical mismatches that accumulate over time.

- A tick did not arrive.

- A reversal did not happen the same way as in the model.

- An action was not triggered in the same event sequence as in the tester.

- An order was not executed at a critical moment.

- An exit happened at a different price or in a different state of the event flow.

At the level of one trade, this may look minor. But for sensitive systems, these small deviations quickly turn into a completely different trading path. At that point, the live EA is no longer the same system that was tested.

This is why forward testing should never be reduced to a simple “profit or loss” check. It is also needed to answer a deeper question: does the real trading path still match the logic that was verified in the tester?

If it does not, the issue may be far more serious than it first appears. The strategy may not have “stopped working.” Its live implementation may simply no longer match the model that was researched.

Why Execution Quality Matters in Forward Testing

This is one of the most practical conclusions in the entire discussion.

Very often, when a strategy performs worse during forward testing, the trader assumes the market simply changed. Sometimes that is true. But in many cases, the real reason lies elsewhere: in execution quality.

Once the system enters live conditions, many things can destroy the math of an otherwise valid idea: rejects, partial fills, differences between virtual and real trading logic, order-processing delays, changing spread, rollover effects, and differences in how market and limit orders are handled.

For execution-sensitive systems, these are not secondary details. They are the core of the problem. A beautiful backtest may become almost useless if live orders are not executed in the way the model assumed. That is why forward testing is also a test of whether the strategy is executable in practice, not only whether it is profitable in theory.

This is a critical shift in understanding. Forward testing an expert advisor is important not simply because it shows what the system may earn on the next market segment. It is important because it reveals whether execution destroys the strategy’s internal mechanism.

Why Real Ticks Are Critical

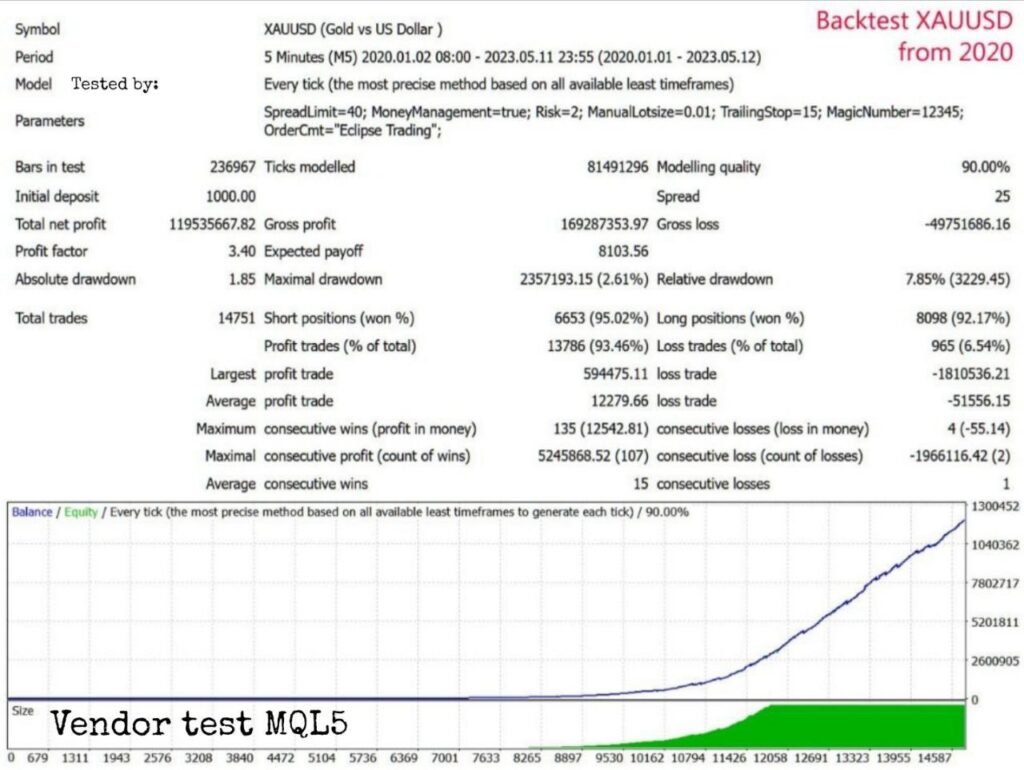

If a strategy is sensitive to tick-level behavior, then rough testing modes can create dangerous illusions. This becomes especially obvious in systems that look excellent on generated ticks but deteriorate sharply on real ticks.

A good example of a vendor test in the MetaTrader 4 terminal with 90% quality and low quality tick history:

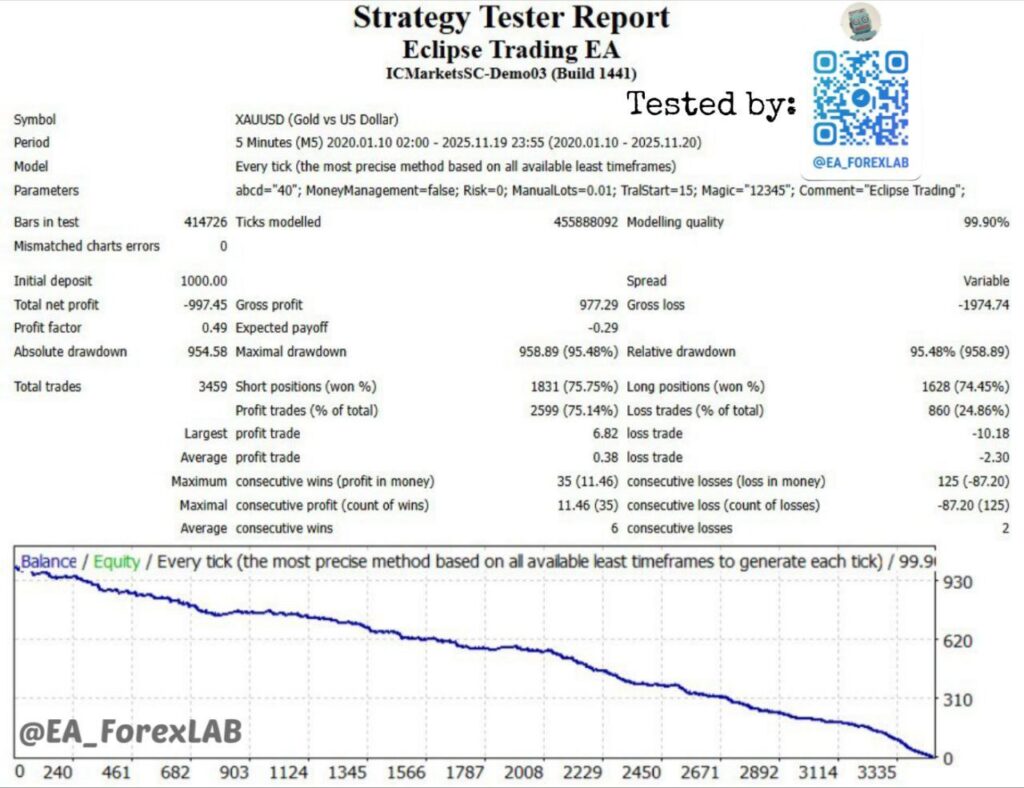

Test MT4 Tick Data Suite 99% Real Spread with the highest quality tick history from broker Darwinex:

This affects forward testing as well. The value of forward testing depends heavily on the quality of all prior research. If the strategy was originally studied in an overly rough model, then the forward stage already stands on a weak foundation.

That is why good forward testing cannot be separated from the subject of real ticks. It should be the continuation of a research process that was built as close to real trading conditions as possible from the start.

The practical meaning is simple: the weaker the model before forward testing, the less confidence you should have in the forward test itself. If the strategy received a false sense of credibility in the tester, then the next validation stage is already contaminated by that distortion.

Why One Good Out-of-Sample Period Can Be Misleading

Traders naturally enjoy finding confirmation. The problem is that a single successful out-of-sample period can very easily become a tool of self-deception.

A favorable segment may have been chosen by accident. The process may have been structured in a way that weak parameter sets were filtered out while attractive ones were kept. The OOS period may simply have been a segment where almost any reasonable system would have looked profitable.

That is exactly why one forward test should never be treated as a seal of quality. It may be a useful signal, but by itself it does not protect against selection bias, luck, or subtle forms of looking into the future.

A serious research process begins when a trader stops searching for confirmation and starts searching for reasons to doubt the result.

Why Walk-Forward Testing Is More Honest Than a Single Forward Test

This is where walk-forward testing becomes especially valuable.

A one-time optimization plus one forward period can look promising, but walk-forward testing usually gives a picture that is much closer to real operation. Yes, it often looks less beautiful. But it is also more honest.

Walk-forward testing is useful because it forces the strategy to go through a repeated cycle: optimize, test on the next segment, re-optimize, test again. This makes it much harder to hide behind one lucky period. It gives a better picture of how the strategy might behave in real life, where the market keeps changing and the trader does not get to live inside one attractive historical fragment.

Put simply, a single forward test answers: “maybe?”

Walk-forward testing gets much closer to: “how is this likely to behave in actual use?”

That is why walk-forward testing usually gives a less glossy but more truthful view of future behavior.

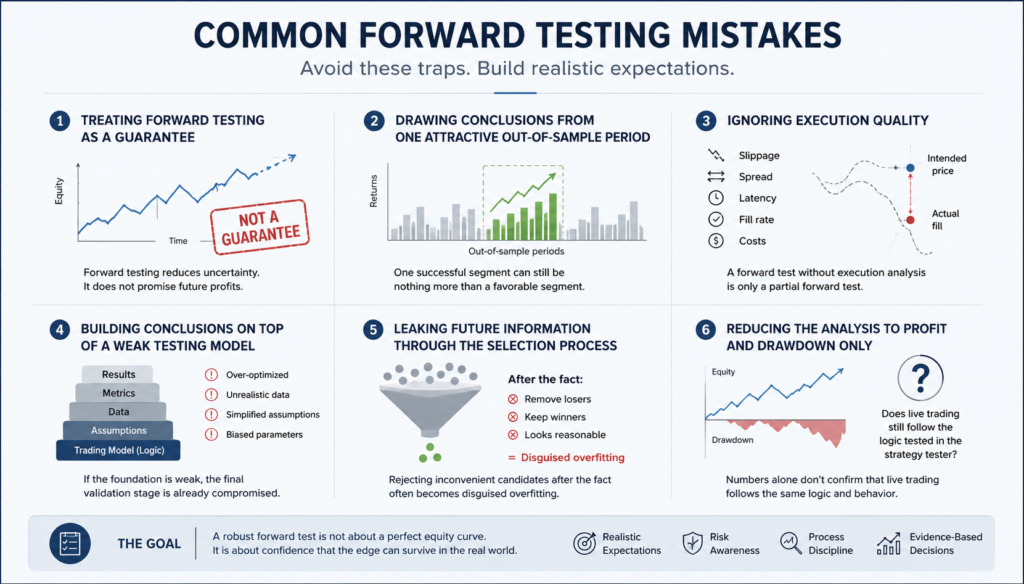

Common Forward Testing Mistakes

There are several mistakes traders make again and again.

The first is treating forward testing as a guarantee. It is not a guarantee. It does not promise future profit. At best, it reduces uncertainty if done honestly.

The second is drawing conclusions from one attractive out-of-sample period. One successful segment can still be nothing more than a favorable segment.

The third is ignoring execution quality. A forward test without execution analysis is only a partial forward test.

The fourth is building conclusions on top of a weak testing model. If the system was studied in an unrealistic framework before forward testing, then the final validation stage is already compromised.

The fifth is leaking future information through the selection process. Rejecting inconvenient candidates after the fact often looks like reasonable filtering, but in reality it becomes disguised overfitting.

The sixth is reducing the entire analysis to profit and drawdown while ignoring whether the live trading path still matches the logic tested in the strategy tester.

What Forward Testing Should Prove Before Live Deployment

Before a strategy is trusted with real money, forward testing should help answer several practical questions.

- Does the expert advisor remain stable outside the training sample?

- Does the live behavior still match the logic validated in the tester?

- Does execution degrade the system’s edge?

- Do broker and platform conditions distort the strategy?

- Is the system too sensitive to infrastructure such as symbol, server, VPS, or trading hours?

- Does the research process still look trustworthy after this additional layer of validation?

That is the correct role of forward testing. It does not prove perfection. It proves whether the system deserves the right to move one step closer to live deployment.

Conclusion

Forward testing an expert advisor is important not because it provides a comforting screenshot after optimization. Its real purpose is to verify whether the logic discovered in the strategy tester can survive in an environment where everything becomes harsher: real ticks, real execution, real platform limitations, and real implementation errors.

That is why forward testing shows more than most traders think. It does not only show profit or loss. It shows robustness, overfitting risk, tradability, execution sensitivity, engineering correctness, infrastructure sensitivity, and the level of trust you can place in the entire research chain.

A strong algorithmic trader is not the one who finds the most beautiful backtests. A strong algorithmic trader is the one who understands that between a good backtest and a real trading system, there must be an honest forward test.

You can see a catalog of advisors that we tested with real spreads on high-quality tick history on this page.

Subscribe to our channel, here you will find the best 👇